If you read my last newsletter you may have some questions. I sort of just jumped right into my story and experience to give myself some credibility and share with you guys what real world real estate investing looks like vs what you may have imagined.

In this weeks newsletter I wanted to give you guys sort of the basics of real estate investing to give you a better idea of what it means to invest in real estate and how to do it and how to set goals around it.

Appreciation

Historically, investing in real estate has been a good way to build wealth over the long term. However, it's important to note that past performance is not necessarily indicative of future results.

It's worth noting that investing in real estate is not without risks. For example, if the local housing market declines or if the owner experiences financial difficulties, it may be difficult to sell the home or refinance the mortgage.

Therefore, it's important to carefully consider all of the factors before making a decision to buy real estate and to be prepared for the potential risks and responsibilities that come with it.

There are several factors that can affect the value of a home, such as the location, local economic conditions, and the state of the housing market.

One of the main reasons that buying real estate can be a good investment is that it can appreciate in value over time. As the value of a home increases, the owner can potentially sell it for a profit or use the increased value as collateral for a loan (leverage).

Below is a chart from the Federal Reserve Bank. (https://fred.stlouisfed.org/

|

The name of the game is owning appreciating assets that pay for themselves. Meaning own real estate using someone else’s money so you have as little invested as possible and have that real estate produce an income that exceeds the debt you owe on it. This lets you assume all of the appreciation from the property and the income produced is also paying down the debt owed on the property. In my opinion, these are the two most important aspects of RE investing. Any additional cash flow is the cherry on top.

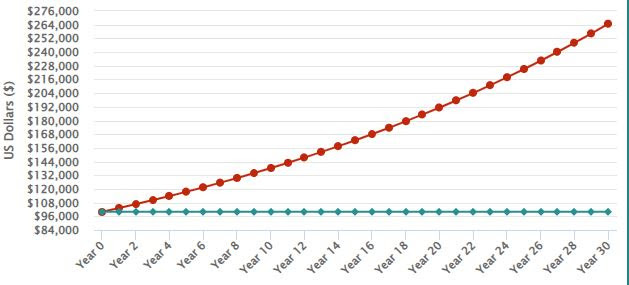

Investing in RE is a long term game. You maybe thinking that flipping properties is the way you want to go… I would argue that flipping properties could make you rich but it will not build you wealth. The goal here is to buy property and hold it for 10-30 years. The average real estate appreciation in the United States has varied significantly over the past 30 years. According to the National Association of Realtors, the average annual appreciation rate for single-family homes was 3.3% between 1991 and 2021. This appreciation compounds year over year. Below is a graph of what 3.3% appreciation looks like on a $100,000 investment that you hold for 30 years.

|

Debt Paydown

Now imagine, if you don’t refinance the property and you just pay your minimum mortgage payment every month, you’re at year 30, your mortgage is paid off and now you own a $270,000 asset that is still collecting an income and all you had invested was your initial 20% down ($20,000). That is a 1250% return on your investment! That is appreciation. Now remember, you didn’t pay any of those mortgage payments, your tenant did and you got a little more in rent than what your mortgage costs, see how this works? That’s the power of debt paydown.

Leverage

Let’s also look at the power of leverage. Leverage is when you refinance the property to get the equity out and use to invest into another property. So lets say every 5 years you refinance and cash out $20,000. You won’t have a paid off house in 30 years but what you will have is the capital to invest every 5 years into another $100,000 house. that means in 30 years if you didn’t use any more of your own personal capital you could cash out $100,000 from this one property and that could buy you 5 more houses that you could do the same thing with. This gets big. This is the power of long term holding real estate. When you flip there are also additional costs associated with selling properties including capital gains tax. This is money that you don’t have to spend if you don’t sell the property. The money you get when you cash out refinance a property is tax free.

Now that we have looked at appreciation and holding vs flipping lets dive into cashflow.

Cash Flow

Cash flow is the amount net income you make off the property each month. Rent - Expenses. A lot of beginner investor think that the mortgage is the only expense that you may have as a rental property owner and this is far from the truth.

When calculating the cash flow of a rental property, it is important to consider all of the expenses associated with owning and operating the property. Some of the most common expenses to consider include:

-

Mortgage payments: If the property is financed with a mortgage, the mortgage payments will be a significant expense to consider.

-

Property taxes: Property taxes are typically paid on an annual basis and should be accounted for in the cash flow calculation.

-

Insurance: It is important to carry insurance on the rental property to protect against potential losses. The cost of insurance should be included in the cash flow calculation.

(Most of the time Property taxes and Insurance will be part of the mortgage payment we call this conglomeration (PITI- Principal, Interest, Taxes, Insurance)

-

Maintenance and repairs: The property will need to be maintained and repaired on an ongoing basis, and these expenses should be accounted for in the cash flow calculation.

-

Property management fees: If you hire a property management company to handle the day-to-day operations of the rental property, their fees should be included in the cash flow calculation.

-

Vacancy and credit loss: It is important to account for the possibility of vacancies and credit loss in the cash flow calculation. This can be done by setting aside a percentage of the rent for these contingencies.

By accounting for all of these expenses in the cash flow calculation, you will be able to get a more accurate picture of the profitability of the rental property.

It can be challenging to estimate vacancy and maintenance expenses for a rental property, as they can vary widely depending on a number of factors such as the age and condition of the property, the location, and the quality of the tenants. That being said, it is generally a good idea to set aside a percentage of the rent for vacancy and maintenance expenses.

As a general rule of thumb, you can estimate vacancy expenses by setting aside between 5% and 10% of the rent for this purpose. This will allow you to cover the cost of any periods of vacancy that may occur.

In terms of maintenance expenses, it is generally a good idea to set aside between 1% and 3% of the property's value each year for this purpose. For example, if the property is worth $200,000, you should set aside between $2,000 and $6,000 per year for maintenance expenses.

Keep in mind that these are just rough estimates and you may need to adjust your estimates based on the specific circumstances of your rental property. It is always a good idea to keep track of actual expenses as they occur so that you can adjust your budget accordingly. When I evaluate rental properties I typically use 15%-20% to account for maintenance and vacancy together.

Here is an example: You purchase a $100,000 property at a 7% interest rate. And you rent it out for $1,200. You put 20% down so your loan is $80,000. Your principal and interest payment for the mortgage would be $665.3. Estimate property taxes at $1,800 a year and insurance at $1,300 a year. You total PITI would be $965.30. Now you have to estimate 15% of rent ($1200) to save back for maintenance and vacancy this is $180. So you total expense is $1145.3 per month. Your rent is $1,200 a month. You are cash flowing $54.7 every month.

How do you know if this is a good investment? Well let’s look at what you are investing vs what you are getting in return.

Cash on Cash Return

Cash on cash return is a measure of the return on an investment, specifically on real estate investments. It is calculated by dividing the annual cash flow of an investment by the total amount of cash invested in the investment. The cash flow is the amount of money that the investment generates after all operating expenses, such as mortgage payments, insurance, property taxes, and repairs, have been paid.

Cash on cash return is often used by real estate investors to compare the potential returns of different properties and to assess the overall performance of their real estate portfolio. It is important to note that cash on cash return does not take into account the appreciation of the property or any other non-cash factors, such as tax benefits, that may affect the overall return on the investment.

Here's an example of how to calculate cash on cash return:

Looking at the above example you’ve invested $20,000 in a rental property that generates $656.4 in annual cash flow. To calculate the cash on cash return, you would divide the annual cash flow by the total amount invested:

Cash on cash return = $656.4 / $20,000 = 3%

In this example, the cash on cash return is 3%. This means that the investment is generating a 3% return on the cash invested. So is 3% a good return on your investment?

There is no one-size-fits-all answer to this question, as the definition of a "good" cash on cash return will vary depending on the individual investor's goals and risk tolerance. Some investors may be satisfied with a lower cash on cash return if the investment has a lower level of risk, while others may be willing to accept a higher level of risk in exchange for the potential for a higher return.

In general, however, a cash on cash return of 8-12% is often considered to be a good return for a rental property, although this can vary depending on the local real estate market and the specific characteristics of the property.

It's also worth noting that a higher cash on cash return is not always better, as it may indicate a higher level of risk or a higher level of effort required to manage the property. As with any investment, it's important to carefully consider the potential risks and rewards before making a decision.

This means when analyzing this deal before you buy it you know you either have to get a discount on the purchase price or you want to find comps that would support that you could get more than $1,200 rent for this property, or find a different way to invest less in the deal (small down payment, less rehab).

That is a ton of info to read through! If you made it this far I commend you and thank you for following my newsletter! Next week we will dive into Analyzing a Deal and how to know if its a good investment before you purchase it! Subscribe down below or share with a friend that you think may find some value in this!